Key factors influencing the language travel market for 2021

- Demand for language travel remains strong but practical considerations – vaccination rates, travel restrictions, flight availability, and more – will determine the pace of recovery in the study travel sector this year

- In the meantime, schools and service providers can anticipate a more varied and segmented marketplace in 2021, with an even greater interest in value-added programming

In a readout from the January 2021 edition of StudyWorld, English UK Business Development Director Tim Barker highlighted some of the key takeaways from the virtual event.

While Mr Barker's remarks were focused on the outlook for the ELT sector in the UK, they can be broadly applied to most other major destinations for language travel.

Demands remains strong

In an echo of the pattern that has followed other major disruptions in recent history, English UK observes that there is strong pent-up demand for language travel.

"The second half of the year should see a significant bounce back," says Mr Barker. "Across the board, there is a sense that young people face frustrations at their lack of opportunities this year and are desperate to travel again."

Results will vary

There are of course a number of underlying variables that will influence the timing and pace of recovery, including the progress of vaccination efforts in both sending and destination countries, the resumption of international flight services, and the availability of in-person instruction.

"Recovery will be market-specific," says Mr Barker, "and it will not be uniform." In some key markets – China and Korea, for example – recovery in student mobility is not expected to take hold until the second half of 2021. Other markets may be impacted by specific travel restrictions between countries, including quarantine requirements.

Time for value adds

It has been widely observed that the pandemic has had an accelerating or amplifying effect on a number of trends that have been active in the industry for some time – the rapid and widespread adoption of online learning being perhaps the best example of this.

But English UK highlights as well the trend toward specialised programmes and services for language travel students. "It is more critical than ever to add value to the ELT experience," says Mr Barker. Improvements in domestic ELT provision in key sending markets, and a corresponding increase in proficiency for students, as well as a declining average length of stay for many students, have put this trend into even sharper focus.

Think "English and…" where the "and" might be sports training or art or academic courses. Or perhaps distinct social or cultural opportunities, or exam preparation or any other features targeted to increasingly segmented cohorts of students.

This is partly a function of differentiating school and agent offerings in an intensely competitive marketplace. But there is another aspect at play here as well in that students and families are increasingly looking for new experiences and for even better value in their programmes abroad.

Strengthening the agent channel

English UK highlights as well the continuing critical role of education agents in recruitment for language programmes. Mr Barker notes that in some markets, such as China, the agent supply chain may have been impacted by a hollowing out of the sub-agent network as smaller agents have been forced to scale back or wind up operations during the pandemic.

The sector has proven to be very resilient, however, and a February 2021 webinar by market research specialists Bonard observes that an estimated 80% of mid to large-sized agencies in China are continuing operations, and that optimism is building among agencies in 2021. The volumes of student inquiries in China are also reportedly holding steady in recent quarters and nearly all responding agencies are planning to send students abroad as of fall 2021, if not earlier.

Looking to summer

The big question in every major language travel destination is what can be expected for the upcoming peak season – meaning the key summer months for Northern Hemisphere providers.

"There might be a summer," concludes Mr Barker. "But it will be late and inconsistent." That is to say, that student bookings can be expected to be later than usual and are going to demand a great deal of flexibility on the part of schools and service providers. Students and parents will need considerable reassurance around health and safety measures as well, and flight availability and pricing will be a huge question mark.

This observation reflects a growing body of opinion that, especially given the overall progress of ongoing vaccination efforts, larger-scale student mobility will only really begin to recover in the latter months of this year. This may be especially true for new bookings, commencing students, and juniors.

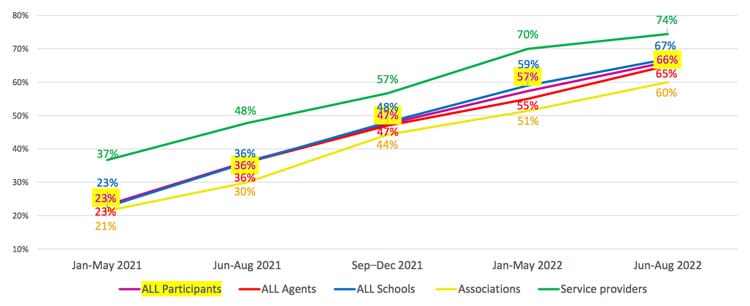

The latest pulse survey from ALTO (the Association of Language Travel Organisations) gathered updated survey responses from agents, schools, associations, and service providers in January 2021. This follows two earlier pulse cycles in July and October 2020, and, while the results vary somewhat from survey to survey, the overall industry outlook is reasonably stable.

However, we do see a softening of expectations in terms of business recovery in the latest ALTO survey. The following chart reflects the outlook of the language travel sector as of January 2021, with respondents, on average, expecting to recover half of pre-pandemic business volumes by the end of 2021 and roughly two-thirds by summer 2022. This compares to the October 2020 survey cycle where respondents anticipated a roughly 50% recovery by summer 2021 and then to be closer to the two-thirds mark by May 2022.

For additional background, please see: